Building open infrastructure database for the GCC.

GulfInfra is an independent research firm building an open-access infrastructure database for the GCC. We track every disclosed PPP procurement across water, power, desalination, sewage, transmission, waste-to-energy and district cooling - tariffs, winning consortia, prequalified bidders, runner-up bids, financing and timelines.

What we are doing

GCC PPP is one of the most active infrastructure markets in the world, but the data lives in paywalled newsletters and the heads of a few specialists. Bidders price deals without knowing the runner-up tariff. Lenders can't see the full track record. We collect public sources, normalise them, and publish the benchmark for free. Seven industries, 136 procurements, 1999-2030.

Methodology

100% open-source data, verbatim from procurer announcements and reputable trade media. Every non-trivial claim carries at least two independent source links; where a figure isn't publicly disclosed, the row says so. Full source list and verification rules: read the methodology →

This is the GulfInfra database - compiled from publicly available sources to capture the main information about the GCC infrastructure industry. The sidebar groups the work into three sections: Database, Pipeline and Reference.

1. Database

Everything you need to map a GCC infrastructure PPP transaction - seven industries with structured deal records, plus four directories that index every entity touching those deals.

Industries - research tables across seven sectors (ISTP, IWPP, SWRO, Solar IPP, Waste-to-Energy, IWTP, District Cooling). Each deal carries tariff, capex, full bidder lineup, winning consortium with equity split, procurement timeline (RFQ → RFP → bids → preferred bidder → financial close → COD) and source links.

Developers - the developers / EPC contractors / O&M operators competing for concessions. Every sponsor profile shows the deals they have bid on, won or participated in, partnership network and win-rate.

Procurers - the government off-takers running the tenders: SWPC, EWEC, KAPP, PIF, Ashghal, OPWP, NWS and the rest. Each profile lists every deal tendered, by year, with the winner attached.

Advisors - five branches: financial, model audit, legal, technical, plus insurance + environmental. Profiles show the mandates each firm held on the procurer, sponsor or lender side.

Banks - the commercial and development-finance lenders providing project debt - tenor, tranche structure and margin where disclosed.

How the parties fit together

A typical GCC PPP transaction is built around the SPV (project company). The government entity (procurer / offtaker) holds the concession agreement with the SPV and makes availability or tariff payments over the concession term; debt + equity financing flow in from the left; the SPV contracts out construction and operations to the EPC and O&M contractors, who hold an interface agreement between them.

2. Pipeline

Forward-looking surfaces - what's in market, what's been announced, and what's being reported.

Tenders - live procurements grouped by stage (EOI / RFQ / RFP / Bid Submission / Preferred Bidder / Financial Close) plus the announced pipeline that hasn't reached EOI yet.

News - curated deal-flow items from MEED, IJGlobal, The National, Zawya, Reuters, Argaam and sponsor / lender press releases.

3. Reference

Articles - long-form analysis on PPP economics, project finance, bidding strategy, equity IRR, force majeure and the geopolitics shaping GCC tariffs.

Glossary - terminology used across the GCC infrastructure industry: contract types, procurement stages, financing structures, technology acronyms.

Project finance industries

Below are the most popular project finance industries in the Middle East. Click.

An Independent Sewage Treatment Plant (ISTP) is a municipal wastewater facility that receives raw sewage from a city's collection network and converts it, in a continuous flow process, into treated sewage effluent (TSE) clean enough to reuse for irrigation, landscaping, district cooling make-up water and industrial processes. A large GCC ISTP processes 100,000 to 600,000 cubic metres per day - the daily wastewater output of a city of roughly half a million to three million people.

How an ISTP fits in the city water cycle

A high-level view of how municipal wastewater moves through an ISTP and back into the city as treated effluent.

City & homes

Households, offices, hotels and industry where the city's wastewater originates.

Sewer network

The buried collection grid that carries wastewater from buildings to the ISTP inlet.

The treatment plant itself

Where raw sewage is converted into reusable treated effluent.

Reuse network

Pipework that distributes treated sewage effluent (TSE) back into the city for non-potable uses.

Sludge handling

Biomass settled out of the treated water. Dewatered, dried and shipped offsite for disposal or beneficial reuse.

How is the sewage treated?

From raw influent to reusable effluent in five steps.

Click any step in the flow above

Each step opens a short description here. The same five-step backbone runs in every ISTP - what changes between deals is the technology chosen at the secondary and tertiary stages.

What different technologies are used for this?

Technology

What it is

How often it is used

Conventional Activated Sludge

CAS

The old, reliable workhorse. Big open tanks where natural bacteria eat the dirt in the water, then settle to the bottom and clean water flows on. Easy to build, cheapest to run, but takes a lot of land.

Most used

Membrane Bioreactor

MBR

A modern, compact version. Same bacteria as CAS, but the clean water is squeezed out through very fine sieves (membranes) instead of letting it settle. The plant fits on a much smaller site and the water comes out cleaner, but the membranes wear out over time and cost more to run.

Often used

Biological Nutrient Removal

BNR / EBPR

A version of CAS that also strips out nitrogen and phosphorus - the chemicals from fertilisers and detergents that cause algae blooms in rivers and seas.

Sometimes used

Sequencing Batch Reactor

SBR

One tank that does everything in turns - fills up, treats, lets the dirt settle, then empties. Like a washing-machine cycle. Good for smaller plants but doesn't scale up to city size.

Rarely used

Moving Bed Biofilm Reactor

MBBR / IFAS

Small plastic chips floating in the tank that bacteria stick to and grow on. Lets you cram more cleaning into less space - often used to upgrade an old plant without building new tanks.

Sometimes used

Real-world examples

Operational ISTPs from the research dataset.

Dammam West Saudi Arabia

Capacity

200,000 m³/day

Technology

CAS + tertiary filtration

Consortium

Metito + Mowah + Orascom

Operational since

2022 (built 2018-2022 under a 25-year BOOT)

Serves

Dammam metro area, Saudi Arabia's Eastern Province

A classic conventional activated sludge layout - two large round secondary clarifiers in the foreground, rectangular aeration basins behind, admin and chemical buildings along the back. Treated effluent is reused for landscape irrigation across the Eastern Province.

Madinah-3 Saudi Arabia

Capacity

200,000 m³/day (expandable to 375,000)

Technology

Waterleau MBR (membrane bioreactor)

Consortium

Acciona + Tawzea + Tamasuk

Operational since

Q4 2024 (built 2021-2024 under a 25-year BOOT)

Serves

The holy city of Madinah and surrounding districts

One of the newest ISTPs in the GCC and the first to use Waterleau MBR at this scale. The aerial photo shows the discharge outfall - treated effluent flowing out through a turquoise-tiled channel into a polishing pond before being sent to irrigation.

Muharraq Bahrain

Capacity

100,000 m³/day

Technology

CAS + nutrient removal + sludge incineration

Consortium

Samsung Engineering (now Almar)

Operational since

2014 (built 2011-2014 under a 27-year BOO)

Serves

Muharraq island and northern Bahrain

A compact, fully enclosed plant on reclaimed land at the edge of the Gulf. The buildings hide most of the equipment - aeration tanks, clarifiers and tertiary filtration all sit inside the white halls. It is the only GCC ISTP with an on-site sludge incinerator, which turns the leftover sludge into ash for safe disposal.

Sulaibiya Kuwait

Capacity

600,000 m³/day (roughly the daily output of Kuwait City)

2004 (built 2002-2004 under a 30-year BOT, retrofitted 2015-19)

Serves

Greater Kuwait City and surrounding governorates

The first large-scale plant in the world to polish sewage all the way back to near-drinking-water quality using reverse osmosis - and still one of the biggest of its kind by capacity. The bulbous tanks in this photo are part of the membrane filtration line, the heart of the plant.

Database

Current research on independent ISTP tariffs based on the selected projects.

Sewage Treatment Plants in GCC

1 Final tariff against plant capacity

Awarded GCC ISTPs · tariff against plant capacity, categorised by RFP submission date

2 Bigger plants cost less per m³/d - economies of scale

Project cost divided by capacity, against plant size · Project cost = EPC + financing cost till COD + other cost till COD

3 Who is winning the market - sponsor participation

Tracked capacity per sponsor · every named consortium member counted on each deal they won

4 Bid ladder - winning vs runner-up tariffs

L1 (winner), L2 (next-lowest losing bid) and L3 (third-lowest) on the same tariff axis · the wider the spread, the less competitive the field

5 Equity structures

Ownership split where disclosed (%)

6 Where the market is - by country

Tracked capacity and project count by country

7 Process technology mix

Treatment process by project · TBC = not yet specified at bid

8 How long does an ISTP take - RFP to operation

Years from RFP issue to commercial operation · click a bucket for the project list

9 Who shows up at RFQ - top 15 prequalification participants

Number of GCC ISTP deals each name appeared in the RFQ shortlist for

10 Who finances ISTPs - top lenders by deal count

Number of GCC ISTP deals each bank participated in (financing tranche unknown)

11 Bidder funnel - prequalified vs final

Competition health, on deals where the funnel is publicly disclosed

A traditional IPP (Independent Power Project) is a large gas-fired power station, owned by a private company, that sells its electricity to the national grid under a long-term contract - typically 20 to 25 years at a fixed price per kilowatt-hour. A single modern Gulf plant produces 1.5-2.4 GW, sufficient to supply approximately 1.5 million homes.

In the Gulf today, the majority of new traditional IPPs use one of two technologies: CCGT for base-load electricity, and OCGT for fast-start "peaker" plants that operate during demand spikes. Coal and oil-fired plants remain only as legacy assets (Hassyan has since been converted to gas) and no new ones are being commissioned. Renewable power plants such as solar and wind use the same commercial structure but are covered under Renewable Energy; plants that bundle power with drinking water are covered under IWPP.

How an IPP fits the national power grid

The plant sits between the fuel supply (gas in most GCC deals; HFO, diesel or coal historically) and the high-voltage transmission grid (electricity out).

Main technologies: CCGT and OCGT

There are two principal methods to convert natural gas into electricity, and the key difference is the treatment of the residual heat.

OCGT (open-cycle gas turbine) combusts gas, drives a single turbine, generates electricity, and exhausts the hot flue gas directly to the stack. Inexpensive to build and rapid to start, but more than half of the fuel's energy is lost as waste heat. Today OCGT is primarily used as a "peaker" - a smaller plant that operates only for short periods during demand spikes.

CCGT (combined-cycle gas turbine) follows the same initial path, then captures that hot exhaust to boil water and drive a second turbine. The additional stage approximately doubles the useful output: efficiency rises from around 38% (OCGT) to around 60% (CCGT). This is the default technology for the majority of new large Gulf power plants.

A short history. Until the late 1990s, OCGT was the default across the Gulf - natural gas was inexpensive at the wellhead, leaving little economic incentive to pursue higher efficiency. CCGT subsequently displaced OCGT in two waves: approximately 2000-2007 at plants such as Taweelah, Shuweihat and Fujairah (~58% efficient), and again from 2018 with larger and higher-temperature turbines at Hassyan, Fujairah F3, Mirfa 2 and Mesaieed (~62% efficient).

The diagram below shows both technologies side by side. The first three steps are identical. After that, OCGT terminates; CCGT continues through two additional steps to recover the residual heat. Click any box to read a description of that step.

Click any step in the flow above

Steps 1-3 are identical between OCGT and CCGT - same compressor, same combustor, same gas turbine. The two technologies diverge at step 4: OCGT exhausts straight to atmosphere; CCGT routes that exhaust into a heat-recovery steam generator to drive a second turbine. That single addition is worth ~22 efficiency points.

Available technologies

Technology

What it is

How often it is used

F-class gas turbines

Large gas turbines from Mitsubishi, Siemens and GE

The dominant gas turbine at Gulf plants from 2000 to 2015. Each unit produces 200-280 MW. Approximately 58% efficient when paired with a steam stage (the CCGT configuration). Deployed at Taweelah A2/B, Shuweihat, Fujairah F1/F2 and Rabigh 1.

Often used

H-class gas turbines

Newer, larger, higher-temperature generation from Mitsubishi, Siemens and GE

The current standard for new builds since 2018. Larger (350-600 MW per unit) and operating at higher internal temperatures (approximately 1,600 °C - the blades use specialised heat-resistant coatings to withstand the conditions). Approximately 62% efficient. Deployed at Hassyan, Fujairah F3, Mirfa and Mesaieed.

Most used

OCGT peakers

Single-stage, fast-start "peaker" plants

Smaller, single-stage gas turbines that operate only during periods of peak electricity demand, where high efficiency is not a priority. Approximately 38% efficient, but low capital cost and operational within minutes. Connected to the same gas pipeline as the larger CCGT plants.

Sometimes used

Black-start & grid services

Restart the grid + keep it stable

Some plants include a dedicated auxiliary generator capable of restarting the entire national grid after a total blackout. The larger CCGTs can also adjust output rapidly to maintain grid frequency stability.

Sometimes used

CCUS-ready design

Space reserved for future carbon capture

The most recent plants (Misfah and Duqm, both awarded in early 2026) reserve plot space and tie-in points on site to permit a future carbon-capture unit to be installed and remove CO₂ from the exhaust.

Rarely used

Real-world examples

Operational and awarded IPPs from the dataset. Where the specific plant photo is not yet on file, a sister plant or complex it occupies is shown instead - flagged in the caption.

Riyadh PP11 / Dhuruma IPP Saudi Arabia

Capacity

1,729 MW

Turbine class

F-class CCGT

Consortium

GDF Suez (now ENGIE) + AlJomaih + Sojitz

COD

2013

Serves

Riyadh, 125 km west of the city

The benchmark Saudi IPP: USD 0.028/kWh tariff at award in 2009 - one of the cheapest CCGT tariffs ever signed in the region at the time.

Hassyan IPP UAE

Capacity

2,400 MW

Turbine class

Gas-fired CCGT (originally tendered as coal)

Consortium

ACWA Power + DEWA + Harbin Electric

COD

Converted to gas; phased COD from 2023

Serves

Dubai grid, ~10% of DEWA generation

Originally awarded 2015 as a 2.4 GW clean-coal IPP - the GCC's first - then converted to gas after Dubai's net-zero pivot. Photo shows the Hassyan coastal complex (Hassyan SWRO in frame); the IPP shares the same coastal site.

Fujairah F3 IPP UAE

Capacity

2,400 MW

Turbine class

H-class CCGT

Consortium

Marubeni + Kepco + ENGIE

COD

2023

Serves

Eastern UAE grid via EWEC

A pure-power H-class plant on the Fujairah complex, next to the older F1/F2 IWPPs. Demonstrates the GCC shift from cogeneration to power-only IPPs as desalination unbundles into RO. Photo shows Taweelah B - a representative F-class CCGT complex on the UAE coast; an F3-specific photo is still to be uploaded.

Photo pending

Plant under construction

Mirfa 2 IPP UAE

Capacity

2,000 MW

Turbine class

H-class CCGT

Consortium

EDF + Sumitomo + Kyushu Electric

COD

Awarded 2024, COD 2027

Serves

Western Region of Abu Dhabi, EWEC

Mirfa 2 carries forward the Mirfa 1 IWPP site as a power-only expansion. EDF's first GCC IPP win. Awarded 2024, plant is under construction - no operational photo exists yet.

What is a desalination (SWRO) plant?

Two distinct concepts to note before reading further:

SWRO is the technology - the desalination process itself (Seawater Reverse Osmosis). Other technologies include MED (Multi-Effect Distillation) and MSF (Multi-Stage Flash); both are heat-driven and largely phased out in new builds.

IWP (Independent Water Project) is the commercial structure - the contract under which a private company owns the plant and sells its water to the national utility under a long-term agreement (typically 20-25 years at a fixed price per cubic metre). The same IWP structure can be applied to any of the three technologies above.

In the modern Gulf, the majority of new IWPs use SWRO, and the two terms are often used interchangeably. The dataset on this tab covers the SWRO-as-IWP fleet.

A Seawater Reverse Osmosis (SWRO) plant converts seawater into drinking water by passing it through plastic membranes whose pores are small enough to permit water molecules to pass while blocking salt ions. To overcome the natural osmotic pressure (~28 bar for Gulf seawater), industrial pumps apply pressures of >60 bar. The output is fresh water from one side of the membrane and twice-concentrated brine from the other. Modern GCC SWRO plants produce 300,000-900,000 m³/day - sufficient drinking water for a major city.

"Independent" means the plant is owned by a private project company and sells output to the national water utility under a long-term water purchase agreement. This tab absorbs what used to be the standalone SWRO page.

How desalinated water fits the city water cycle

Sea in at the left, drinking water out to the city on the right. The schematic shows the four stations.

How a SWRO plant works

Five steps from raw seawater to drinking water. Click any step in the diagram to read a description of that stage.

Click any step in the flow above

Five steps from raw seawater to drinking water. The critical step is the final one - the energy-recovery device that reduced modern desalination costs to a level at which water sells for approximately 30-40 US cents per cubic metre.

Available technologies

Technology

What it is

How often it is used

SWRO

Reverse osmosis through plastic membranes

The standard for every new desalination plant in the Gulf. Drives seawater through plastic membranes at very high pressure; water permeates while salt is blocked. Electricity-driven only; no thermal input. Approximately 2.5-3.5 kWh per cubic metre. Deployed at Hassyan, Taweelah RO, Rabigh-3 and all new builds.

Most used

MED

Boil seawater, reuse the steam (heat-driven)

Heats seawater to approximately 70 °C and boils it across a series of stages, reusing the condensation heat from each stage to drive the next. Economically competitive only where free waste heat from a co-located power plant is available, which is why it was integrated with older IWPPs at Sohar and Salalah. Rarely selected for new builds today.

Rarely used (new builds)

MSF

"Flash" boiling at high temperature (heat-driven)

Heats seawater to 90-110 °C and "flashes" it across multiple low-pressure chambers, condensing the resulting steam to produce fresh water. The earliest Gulf desalination technology (Taweelah A2, Shuweihat S1, Fujairah F1 - all 1999-2007). Phased out due to excessive energy consumption.

Phased out

Real-world examples

Operational SWRO plants from the dataset.

Taweelah RO UAE

Capacity

909,000 m³/day (200 MIGD)

Technology

SWRO + UF pretreatment + PX-Q400 ERD

Consortium

ACWA Power + Mubadala + EWEC

COD

2022

Tariff

USD 0.49/m³ (award 2018)

World's largest single-site SWRO at commissioning. Supplies Abu Dhabi's western and northern grids via EWEC.

Hassyan SWRO UAE

Capacity

818,000 m³/day (180 MIGD)

Technology

SWRO with captive solar PV

Consortium

ACWA Power + DEWA

COD

Phased; full COD 2026

Tariff

USD 0.365/m³ - world record at award May 2023

The world's lowest disclosed SWRO tariff at award. Sited next to Hassyan IPP on the Dubai coastal complex.

Rabigh-3 Saudi Arabia

Capacity

600,000 m³/day

Technology

SWRO on Red Sea intake

Consortium

ACWA Power + Saudi Brothers

COD

May 2022

Tariff

USD 0.53/m³ (world record at award Nov 2018)

Held the SWRO tariff record for ~4 years before Hassyan broke it. Red Sea intake is more sensitive to algal blooms than the Gulf - hence the extra-large UF pretreatment.

Jubail SWRO complex Saudi Arabia

Capacity

Jubail-3A: 600k m³/d · Jubail-3B: 570k m³/d

Technology

SWRO + 61 MW captive solar PV (3B)

Consortium

Jubail-3A: ACWA + Acciona · Jubail-3B: ENGIE

COD

3A: 2023 · 3B: 2024

Twin SWRO procurements on Saudi Arabia's Eastern Province Gulf coast. Jubail-3B is the largest captive-solar desal plant in the GCC at announcement.

What is an IWPP?

An Independent Water & Power Project (IWPP) is the cogeneration bundle: a single plant that produces electricity AND fresh water from the same fuel and the same physical heat cycle. Two technologies in one - the gas-fired power island generates electricity, and the waste or bleed heat from the steam turbine drives a thermal desalination block (MSF or MED) bolted onto the same site. A typical GCC IWPP produces ~2 GW of power and ~500,000 m³/day of fresh water from the same plot.

The "IW" half exists because the GCC has no rivers, almost no rainfall and no large freshwater aquifers. Every drop of municipal water has historically come from the sea via desalination - and the cheapest way to desalinate was to ride the waste heat off a gas-turbine power plant. That's why power and water got bundled into one plant for ~25 years. The current shift is toward decoupling: pure-power IPPs (Tab 1) feed pure-water SWRO (Tab 2) on the same grid, and the new-build IWPP pipeline is thinning out.

How an IWPP feeds both cycles

One fuel input on the left; two product outputs - electricity to the grid AND fresh water to the city. The schematic below shows the dual feed.

How cogeneration couples the two

The story unique to this tab: one fuel input drives a CCGT, and the waste or bleed heat off the steam turbine is what powers the desalination block. Click a step.

Click any step in the flow above

The cogeneration trick is the steam bleed: instead of dumping all the bottoming-cycle heat to the condenser, the IWPP diverts a fraction at the right pressure to drive thermal desalination. That single step is what defines an IWPP versus a power-only IPP.

Cogeneration IWPPs from the dataset - dual-product plants.

Taweelah B UAE

Capacity

2,220 MW · 730,000 m³/d

Power tech

F-class CCGT

Desal tech

MED + MSF

Consortium

Marubeni + JERA + Total + TAQA

COD

2008 (brownfield acquisition)

One of the largest cogeneration IWPPs in the Gulf. Abu Dhabi coastal complex - sits next to Taweelah A1/A2.

Umm Al Houl Qatar

Capacity

2,520 MW · 900,000 m³/d

Power tech

F-class CCGT

Desal tech

MED + RO

Consortium

QEWC + Mitsubishi + JERA + QF

COD

2018

~30% of Qatar's electricity and 40% of its water from one site.

Riyadh PP11 / Dhuruma Saudi Arabia

Capacity

1,729 MW (power-only IPP variant)

Power tech

F-class CCGT

Desal tech

n/a - this site is the IPP referenced for the Saudi tariff benchmark

Consortium

ENGIE + AlJomaih + Sojitz

COD

2013

Included here as the IWPP reference point in tariff disclosure. PP11 itself is a pure IPP - shown for cross-comparison with the cogen plants on either side.

Az-Zour North 1 Kuwait

Capacity

1,539 MW · 107 MIGD (~486k m³/d)

Power tech

F-class CCGT

Desal tech

MED

Consortium

ENGIE + Sumitomo + Al-Sagar

COD

2016

Kuwait's first IWPP under the new PPP framework. Demonstrated the transition-era F+MED template.

Database

Current research on traditional independent power projects (IPP) based on the selected projects.

Traditional power plants in GCC

1 Final tariff against plant capacity

Awarded GCC IPPs · tariff against plant capacity, categorised by RFP era

2 Bigger plants cost less per kilowatt - economies of scale

Project cost per kW against plant size · outliers are typically oil-fired, brownfield extensions, or CCUS-ready newbuilds

3 Who is winning the market - sponsor participation

Tracked capacity per sponsor · every named consortium member counted on each deal they won

4 Equity structures

Ownership split where disclosed (%) · click a row to jump to its project

5 Where the market is - by country

Tracked capacity and project count by country

6 Turbine class mix

Power-island technology by project · TBC = not yet specified at bid

7 How long does an IPP take - RFP to operation

Years from RFP issue to commercial operation · click a bucket for the project list

8 Who finances these projects - top lenders by deal count

Number of GCC IPPs deals each bank participated in (financing tranche unknown)

0 of 0 projects

GulfInfraIndependent power producers (IPP) - GCC

Project

Capacity

Tariff

Winner consortium

Fin. close

Capex

EPC value

Database

Current research on independent water projects (IWP) based on the selected projects. GCC SWRO IWP procurements.

Water power plants in GCC

1 Final tariff against plant capacity

Awarded GCC SWRO IWPs · tariff against plant capacity, categorised by RFP era

2 Bigger plants cost less per m³/d - economies of scale

Build cost per m³/d capacity against plant size · legacy plants and brownfield extensions sit above the trend line

3 Who is winning the market - sponsor participation

Tracked capacity per sponsor · every named consortium member counted on each deal they won

4 Where the market is - by country

Tracked capacity and project count by country

5 Process technology mix

Desalination process by project · SWRO is the new standard

6 How long does an SWRO IWP take - RFP to operation

Years from RFP issue to commercial operation

7 Bid ladder - winning vs runner-up tariffs

L1 (winner), L2 (next-lowest losing bid) and L3 (third-lowest) on the same tariff axis · the wider the spread, the less competitive the field

8 Equity structures

Ownership split where disclosed (%)

9 Who shows up at RFQ - top 15 prequalification participants

Number of GCC SWRO IWPs deals each name appeared in the RFQ shortlist for

10 Who finances these projects - top lenders by deal count

Number of GCC SWRO IWPs deals each bank participated in (financing tranche unknown)

11 Bidder funnel - prequalified vs final

Competition health, on deals where the funnel is publicly disclosed

0 of 0 projects

GulfInfraSWRO Independent water producers (IWP) - GCC

Project

Capacity

Tariff

Winner consortium

Fin. close

Capex

EPC value

Database

Current research on independent water and power projects (IWPP) based on the selected projects. GCC cogeneration IWPP procurements. Most IWPP tariffs are commercially confidential due to the dual-product structure; the tariff scatter shows only Dhuruma/PP11 and Al Dur-2 where the dual split is publicly disclosed. Bubble size = power capacity (MW).

IWPP in GCC

1 Disclosed power tariff against capacity

IWPP tariffs are mostly commercial-confidential. Showing only the disclosed dual splits

2 Bigger plants cost less per kW - bundled cogeneration build cost

Total project capex against power capacity · water block bundled into the same capex line so this measures the joint build

3 Who is winning the market - sponsor participation

Tracked power capacity per sponsor · every named consortium member counted

4 Where the market is - by country

Tracked power capacity and project count by country

5 Power-island + desal technology mix

Each project contributes to a Power tag (gas-turbine class) and a Desal tag (MSF / MED / SWRO hybrid) - bars sum to more than the project count

6 How long does an IWPP take - RFP to operation

Years from RFP issue to commercial operation

7 Bid ladder - winning vs runner-up tariffs

L1 (winner), L2 (next-lowest losing bid) and L3 (third-lowest) on the same tariff axis · the wider the spread, the less competitive the field

8 Equity structures

Ownership split where disclosed (%)

9 Who shows up at RFQ - top 15 prequalification participants

Number of GCC IWPP cogen deals each name appeared in the RFQ shortlist for

10 Who finances these projects - top lenders by deal count

Number of GCC IWPP cogen deals each bank participated in (financing tranche unknown)

11 Bidder funnel - prequalified vs final

Competition health, on deals where the funnel is publicly disclosed

0 of 0 projects

GulfInfraIndependent water & power producers (IWPP) - GCC

Project

Capacity

Tariff

Winner consortium

Fin. close

Capex

EPC value

Renewable Energy

What is a Solar IPP?

A solar power plant is a field of photovoltaic (PV) modules that converts sunlight directly into electricity. Modern utility-scale GCC plants cover 10-40 km² of desert, with millions of glass-and-silicon panels mounted on motorised steel racks that pivot east-to-west through the day to track the sun. There are no moving fluids or thermal cycles - sunlight in, electrons out - which makes PV the simplest and fastest-to-build large power asset on the grid.

The GCC has the world's best solar resource: 2,200+ peak sun hours per year, low cloud cover, high direct irradiance. The cost penalty is heat (silicon cells lose ~0.4% efficiency per °C above 25 °C) and dust (sand accumulation requires robotic dry-cleaning every 1-2 weeks). These are engineering problems already solved.

How a PV plant fits the national grid

Sunlight in at the left, electricity out to the grid on the right. The schematic shows the five stations between the desert and the household.

How a PV plant works

Click any step to read what happens at that stage. The same six-step backbone runs in every utility-scale PV plant. The design choices that move project economics are cell chemistry (CdTe, mono-PERC, TOPCon/HJT), mounting (fixed-tilt versus single-axis tracker), and whether a co-located battery system shifts production into the evening peak.

Click any step in the flow above

Each step opens a short description here. The Solar IPP backbone is identical across every utility-scale GCC plant - the design choices that move LCOE are cell chemistry, tracker share, and whether a BESS is bolted on for evening dispatch.

Silicon module that also captures sunlight reflected off bright desert sand from its rear face - adds 8-12% extra output. Cell efficiency 22-23% on the front. Deployed at Al Dhafra, Sudair and Shuaibah 2 (2020-2023 rounds).

Most used

Mono-PERC

Single-sided silicon module - prior generation

The single-sided version of the bifacial design - no rear-face gain. Cell efficiency 22-23%. Deployed at Sakaka, MBR Phase 3 and Sweihan (2017-2019 rounds), before bifacial became standard.

Higher cell efficiency (24-26%) and better heat tolerance than PERC - hold output better in Gulf summer heat. Replacing PERC in 2024+ rounds. Deployed at Khazna, DEWA Phase 6 and Saudi Round 6.

Often used

CdTe thin-film

Cadmium-telluride layer on glass - no silicon

Cadmium telluride deposited directly on glass. Lower efficiency (19-20%) than silicon, but holds output better in extreme heat. Deployed at DEWA Phase 1 and 2 (2017); rarely chosen since.

Sometimes used

CSP

Concentrated Solar Power - mirrors + thermal storage

Mirrors heat molten salt to 565 °C; the hot salt drives a steam turbine and stores heat for hours, enabling dispatch after sunset. Deployed at DEWA Phase 4 (700 MW + 15 hours storage; the 262.4 m tower is the world's tallest).

Rarely used

Real-world examples

Operational and awarded GCC utility-scale solar IPPs from the research dataset. Scroll through or use the arrows to browse.

Photo pending

Al Dhafra Solar PV

Al Dhafra (DPV2) UAE

Capacity

2,000 MW

Technology

~4M bifacial mono-PERC modules on single-axis trackers, ~20 km²

USD 2.42 c/kWh - the world record at the 2017 award

Serves

Abu Dhabi grid via EWEC

The first GCC project to break the USD 0.03/kWh price floor and the template every UAE round since has built on

Photo pending

Sudair 1.5 GW

Sudair 1.5 GW PV Saudi Arabia

Capacity

1,500 MW

Technology

Bifacial mono-PERC modules on single-axis trackers

Consortium

ACWA Power 35% / Badeel (PIF) 35% / Aramco Power 30%

COD

2024 (25-year BOO)

Tariff

USD 12.39/MWh - then the lowest in Saudi Arabia

Serves

Saudi national grid via SPPC

The largest single-site solar plant in the Middle East at the time of award. Sited in Sudair Industrial City north of Riyadh

Photo pending

MBR Solar Park Phase 5

Mohammed bin Rashid Solar Park Phase 5 UAE

Capacity

900 MW

Technology

~5.7M bifacial modules on single-axis trackers

Consortium

DEWA 51% / ACWA Power 24.5% / Gulf Investment Corporation 24.5% (Shuaa Energy 3 SPV)

COD

Jun 2023 (25-year BOO)

Tariff

USD 1.6953 c/kWh - the then-record tariff at the 2019 award

Serves

Dubai grid via DEWA

One phase of the multi-stage MBR Solar Park at Saih Al-Dahal, targeting 5 GW by 2030. Built in three 300 MW units

Photo pending

Sakaka 300 MW

Sakaka 300 MW PV Saudi Arabia

Capacity

300 MW

Technology

Bifacial mono-PERC modules on single-axis trackers

Consortium

ACWA Power 70% / AlGihaz 30%

COD

Q2 2020 (25-year BOO)

Tariff

USD 23.42/MWh - the world record at the 2018 award

Serves

Saudi national grid via SPPC

Saudi Arabia's first utility-scale solar IPP, sited at Al Jouf in the kingdom's north. The reference deal for the REPDO / SPPC procurement programme

What is a Wind IPP?

A wind IPP is a utility-scale wind farm sold under a long-term power purchase agreement, the same architecture as a thermal or solar IPP. Tall steel towers (110-160 m hub height) carry three-bladed horizontal-axis rotors that turn at 10-20 rpm. Each turbine is a 3-6 MW unit; a typical GCC wind IPP strings together 50-200 of them across a high-wind corridor, with internal medium-voltage collection cables running to a single grid-connection substation.

Where the GCC wind resource sits. Wind energy is concentrated in three corridors: NW Saudi Arabia (Northern Borders, Al Jouf, Madinah - this is where Dumat Al Jandal, Yanbu, Waad Al Shamal and Start sit), central Saudi Arabia (the Al Ghat plateau in Riyadh province, where SPPC awarded a 600 MW round in 2024), and southern Oman (the Dhofar coast and the Khareef monsoon corridor - Dhofar Wind, Duqm, Jaalan Bani Bu Ali). Capacity factors in the best GCC sites reach 35-45%, well above the ~25% global average for onshore wind, because the resource is steadier and the seasonal Khareef monsoon delivers months of constant flow.

Why wind matters in the GCC's renewable mix. Wind generates at night and during the shoulder seasons when PV output is low. A pure-solar grid needs huge batteries to bridge the sunset-to-midnight peak; a solar-plus-wind grid needs much less BESS because the two resources offset each other through the daily cycle. Saudi Arabia's NEOM masterplan and Oman's Vision 2040 both treat wind as the firming complement to PV - the cheapest dispatchable-renewable bundle in the region.

How a wind farm fits the national grid

Wind in at the left, electricity out to the grid on the right. The schematic shows the four stations between the corridor and the household.

How a wind turbine works

Click any step to read what happens at that stage. The same six-step backbone runs in every modern wind turbine. The design choices that differ between deals are the drivetrain (geared versus direct-drive) and rotor scale.

Click any step in the flow above

The same six-step backbone runs in every modern wind turbine. GCC sites favour large rotor diameters with moderate hub heights, optimising for the steady mid-range winds along the NW Saudi corridor and the Dhofar coast.

Available technologies

Technology

What it is

How often it is used

Geared turbines (DFIG)

Vestas V150 / V162 - workhorse of Gulf wind

Doubly-fed induction generator with a multi-stage gearbox. Lower capex, higher maintenance. Vestas V150-4.2 powered Dumat Al Jandal.

Often used

Direct-drive turbines (PMSG)

Goldwind GW155 / GE Cypress - no gearbox

Permanent-magnet generator mounted directly on the rotor shaft - no gearbox. Higher capex, simpler maintenance and longer service intervals. Better for remote or harsh sites.

Sometimes used

Large-rotor turbines

170+ m rotors - higher output in moderate winds

170+ m rotors tuned for sites with steady moderate winds rather than strong gusts. Higher capacity factor for the same hub-height wind speed. Deployed at Dhofar Wind on the Khareef monsoon corridor.

Sometimes used

Hybrid steel-concrete towers

Concrete base + steel top for 130-160 m hub heights

Concrete lower section plus steel tubular section above, reaching 130-160 m hub heights economically. Pioneered at Dumat Al Jandal; now standard at Yanbu and Waad Al Shamal.

Often used

Real-world examples

Operational and awarded GCC utility-scale wind IPPs from the research dataset. Scroll through or use the arrows to browse.

Dumat Al Jandal Saudi Arabia

Capacity

400 MW

Technology

99 Vestas V150-4.2 turbines on hybrid steel-concrete towers

Consortium

EDF Renewables + Masdar

COD

2022 (25-year BOO)

Tariff

USD 0.0213/kWh - the GCC benchmark at the 2019 award

Serves

Saudi national grid via SPPC; sited in Al Jouf province

The first utility-scale wind IPP in the GCC. Set the regional benchmark tariff and proved the hybrid steel-concrete tower template that newer rounds have built on.

Yanbu Wind Saudi Arabia

Capacity

700 MW

Technology

Large-rotor turbines on hybrid towers (consortium TBC at financial close)

Round

SPPC Round 4 (2024 award)

COD

Targeted 2027

Serves

Saudi national grid via SPPC; sited in Madinah province on the Red Sea coast

The largest single-site wind project tendered in the Kingdom to date and one of the largest in the GCC.

Waad Al Shamal Wind Saudi Arabia

Capacity

500-600 MW

Technology

Direct-drive turbines (consortium TBC at financial close)

Round

SPPC Round 4 (2024 award)

COD

Targeted 2027

Serves

Saudi national grid via SPPC; sited in the Northern Borders province

Co-located with the Waad Al Shamal phosphate complex, taking advantage of the Northern Borders corridor's steady winds.

Al Ghat Wind Saudi Arabia

Capacity

600 MW

Technology

Large-rotor turbines (consortium TBC at financial close)

Round

Awarded 2024

COD

Targeted 2027

Serves

Saudi national grid via SPPC; sited on the Riyadh-province plateau

The first wind procurement on the central Saudi plateau, opening a new resource region alongside the NW corridor that hosts Dumat Al Jandal and Yanbu.

Dhofar Wind Oman

Capacity

50 MW

Technology

13 GE 3.83-137 turbines, tuned for the Khareef monsoon corridor

Consortium

Masdar + Rural Areas Electricity Company (Tanweer)

COD

2019 (20-year PPA)

Serves

Salalah and the southern Oman grid

The first utility-scale wind plant on the Arabian Peninsula at commissioning. Built around the Khareef monsoon corridor, which delivers months of constant flow each summer.

What is Storage + Hybrid?

This sub-market covers four overlapping plant types: standalone BESS (battery energy storage system, no generation; arbitrages grid energy and provides frequency response), Solar + BESS (PV plant with co-located batteries that shift midday generation into the evening peak), CSP (concentrated solar power plus molten-salt thermal storage; dispatchable through the night), and Round-the-Clock (RtC) hybrids that combine solar, wind and BESS into a single PPA that delivers firm dispatchable power 24/7.

Why it matters: bridging the duck curve. A solar-heavy grid hits a structural problem at sunset - generation drops to zero between 6 and 9 pm while air-conditioning load still peaks. The cheapest dispatchable bridge is storage. Standalone BESS (Saudi SPPC's Bisha, Najran and Khamis Mushait deals, all awarded 2024-2025) provides 4-8 hours of dispatchable energy at capacity-charge tariffs (around USD 13-15 per kW-month, not per kWh). PV+BESS hybrids embed the storage in the generation PPA. RtC bundles take this one step further: SPPC's RtC1 round in 2025 awarded ~USD 0.048/kWh for 24/7 dispatchable solar-plus-wind-plus-BESS - a tariff competitive with new-build CCGT under a carbon-priced future.

Why CSP still matters in the GCC. CSP capex is roughly 3x that of PV, but its built-in thermal storage (molten salt at 565 °C in two-tank systems) gives 15+ hours of dispatch at a far lower marginal cost than batteries. DEWA Phase 4 (the 700 MW solar tower + trough hybrid in Dubai) demonstrated this at scale: PV + CSP + 15h storage in a single bundled PPA, with PV serving the day and CSP serving the night.

How storage fits the national grid

Solar or wind generation in at the left, dispatchable electricity out to the grid on the right. The schematic shows where storage sits between the two: it absorbs midday surplus and releases it into the evening peak when generation has dropped to zero.

How a storage plant works

Two parallel architectures, one shared grid export. The top three boxes on the left describe a BESS-only or PV+BESS plant; the right column shows the CSP path. Click any step to read what happens at that stage.

Click any step in the flow above

Two parallel architectures, one shared grid export. The PV+BESS path uses electrochemical storage and is the cheapest dispatch bridge. The CSP path uses thermal storage and is the only option that delivers 15+ hours of dispatch at competitive cost without batteries.

Available technologies

Technology

What it is

How often it is used

Li-ion LFP batteries

The default Gulf battery chemistry

The default Gulf chemistry. Better thermal stability than NMC alternatives in 50 °C heat. Typical scale 100-2,000 MWh, 2-8 hour duration. Deployed at Bisha, Najran, Khamis Mushait, Jeddah, MBR Phase 7, Ibri 3.

Most used

Vanadium flow batteries

Long-duration tank-based storage

Electrolyte in external tanks pumped through a cell stack. Decouples power from energy - cheaper per MWh at long durations. Indefinite cycle life. Pilot deployments only; no GCC utility-scale deal disclosed yet.

Rarely used

Sodium-ion batteries

Emerging chemistry - more abundant raw materials

Sodium analogue of Li-ion using abundant raw materials. Cheaper at scale than LFP and more tolerant of high heat. CATL and BYD started commercial production in 2024. Tracked as a 2026-2028 option for the next battery rounds.

Emerging

CSP - parabolic trough

Curved mirrors heating an absorber pipe

Parabolic mirrors focus sunlight onto an absorber pipe. Oil-based HTF (~390 °C) drives a steam cycle; optional molten-salt storage enables night dispatch. Deployed at MBR Phase 4 (600 MW trough) and Shagaya CSP Hybrid in Kuwait.

Rarely used

CSP - central tower

Heliostat field + tower receiver with molten salt

Heliostat field focuses sunlight on a tower receiver running molten salt at 565 °C. Higher cycle efficiency and simpler storage integration than troughs. Deployed at MBR Phase 4 (100 MW tower, 262.4 m - the world's tallest).

Rarely used

Round-the-Clock (RtC) hybrid

Bundled solar + wind + BESS under one 24/7 PPA

One PPA bundling large PV + smaller wind + 4-8 hour LFP battery, sized to deliver firm dispatchable MW 24/7. Replaces a peaker without burning gas. Awarded at SPPC RtC1 in 2025 at ~USD 0.048/kWh - the first round-the-clock PPP at this scale.

Sometimes used

Real-world examples

Operational and awarded GCC storage and hybrid PPPs from the research dataset. Scroll through or use the arrows to browse.

DEWA + ACWA Power + Shanghai Electric (Noor Energy 1 SPV)

COD

Phased; central-tower COD 2023

Tower height

262.4 m - the tallest CSP tower in the world at commissioning

The benchmark large-scale CSP project of the decade. Demonstrated 15-hour dispatch and combined-architecture CSP at utility scale.

Bisha BESS Saudi Arabia

Capacity

Standalone LFP battery system

Duration

4-hour discharge

Round

SPPC standalone-BESS round, 2024 award

Serves

Saudi national grid via SPPC; sited in Asir region

One of the first three standalone-BESS PPPs awarded by SPPC. Capacity-charge tariff structure (USD per kW-month) rather than per-kWh.

Najran BESS Saudi Arabia

Capacity

Standalone LFP battery system

Duration

4-hour discharge

Round

SPPC standalone-BESS round, 2024 award

Serves

Saudi national grid via SPPC; sited in Najran province

Second of the three southern BESS awards. Provides evening-peak dispatch to the south-western Saudi load centres.

Khamis Mushait BESS Saudi Arabia

Capacity

Standalone LFP battery system

Duration

4-hour discharge

Round

SPPC standalone-BESS round, 2024 award

Serves

Saudi national grid via SPPC; sited in Asir region

Third of the cluster of southern standalone-BESS awards, paired with Bisha and Najran to firm up evening dispatch across the region.

MBR Solar Park Phase 7 (PV+BESS) UAE

Capacity

1.6 GW PV + 1,000 MW / 6,000 MWh BESS

Duration

6-hour discharge

Consortium

DEWA-led consortium (final SPV TBC at financial close)

COD

Targeted 2027

Serves

Dubai grid via DEWA

One of the largest PV+BESS bundles ever procured worldwide. Sets the template for storage-paired PV in the next round of the energy transition.

Ibri 3 (PV+BESS) Oman

Capacity

Co-located PV + LFP battery storage

Procurer

OPWP

Serves

Oman national grid; sited in the Al Dhahirah region

Oman's first co-located PV-plus-BESS hybrid deal at scale. Sits on the same Ibri solar corridor as Ibri 1 and Ibri 2.

SPPC RtC1 (Round-the-Clock) Saudi Arabia

Capacity

Dispatchable solar + wind + LFP battery bundle

Tariff

~USD 0.048/kWh at 2025 award

Procurer

SPPC

Structure

Single PPA with firm 24/7 dispatch obligation

The first round-the-clock dispatchable-renewables PPP at scale in the Gulf. Replaces peaker capacity without burning gas at a tariff competitive with new-build CCGT.

Database - Solar IPP

GCC Solar IPP procurements. Tariffs in USD/kWh only - never on the same axis as wind or storage tariffs.

Map - Solar IPP

1 Final tariff against plant capacity

Awarded GCC Solar IPPs · USD/kWh tariff against plant capacity, categorised by RFP era

2 Bigger plants cost less per kilowatt - economies of scale

Build cost per kW against plant size · outliers are typically early-vintage thin-film, CSP hybrids, or PV+BESS

3 Who is winning the market - sponsor participation

Tracked capacity per sponsor · every named consortium member counted on each deal they won

4 Where the market is - by country

Tracked capacity and project count by country

5 PV technology mix

Module / mounting / hybrid classification · counted across the dataset

6 How long does a Solar IPP take - RFP to operation

Years from RFP issue to commercial operation

0 of 0 projects

GulfInfraSolar IPP - GCC

Project

Capacity

Tariff

Winner consortium

Fin. close

Capex

EPC value

Database - Wind IPP

GCC Wind IPP procurements. Tariffs in USD/kWh only.

Map - Wind IPP

1 Final tariff against plant capacity

Awarded GCC Wind IPPs · USD/kWh tariff against plant capacity, categorised by RFP era

2 Bigger plants cost less per kilowatt - economies of scale

Build cost per kW against plant size

3 Who is winning the market - sponsor participation

Tracked capacity per sponsor

4 Where the market is - by country

Tracked capacity and project count by country

5 Turbine technology mix

Drivetrain family (geared DFIG vs direct-drive PMSG vs high-altitude low-wind)

6 How long does a Wind IPP take - RFP to operation

Years from RFP issue to commercial operation

0 of 0 projects

GulfInfraWind IPP - GCC

Project

Capacity

Tariff

Winner consortium

Fin. close

Capex

EPC value

Database - Storage + Hybrid

GCC Storage and Hybrid procurements. RtC and CSP deals carry a USD/kWh tariff; standalone BESS deals carry a capacity charge instead - shown as "capacity charge" in the table where the per-kWh value is not the right unit.

Map - Storage + Hybrid

1 Disclosed energy tariff against plant capacity

Awarded GCC Storage + Hybrid · only deals with a per-kWh PPA tariff shown (RtC + CSP + PV+BESS bundles)

2 Bigger plants cost less per kilowatt - economies of scale

Build cost per kW against plant size · CSP at the top, standalone BESS in the middle, PV+BESS at the bottom

3 Who is winning the market - sponsor participation

Tracked capacity per sponsor

4 Where the market is - by country

Tracked capacity and project count by country

5 Plant technology mix

Standalone BESS / PV+BESS / CSP / RtC bundles classified across the dataset

6 How long does it take - RFP to operation

Years from RFP issue to commercial operation

0 of 0 projects

GulfInfraStorage + Hybrid - GCC

Project

Capacity

Tariff

Winner consortium

Fin. close

Capex

EPC value

Waste Management

What is a Waste-to-Energy plant?

A Waste-to-Energy (WtE) plant is a factory that burns municipal solid waste - household rubbish - at over 1,000 °C to make electricity. Rubbish replaces coal or natural gas as the fuel. The heat boils water to steam, the steam drives a turbine, the turbine drives a generator. The result: 70-90% of a city's landfill is avoided, and every ~30-40 kg of waste produces 1 kWh of electricity exported to the grid.

WtE is one of the most heavily-regulated industrial processes in the world because uncontrolled waste combustion produces dioxins, furans, NOx, SO₂, HCl, mercury and particulates. Modern plants use 4-5 stages of flue-gas treatment to drive emissions well below European IED 2010/75/EU limits. Done properly, the bottom-ash residue (15-25% of input mass) is inert enough to use as road sub-base aggregate.

Real-world examples

Operational and awarded GCC Waste-to-Energy plants from the research dataset. Scroll through or use the arrows to browse.

Sharjah Waste-to-Energy Phase 1 UAE

Throughput

~822 t/d (~300 kt/y) / 30 MW gross

Technology

Mass-burn moving grate (CNIM / Martin)

Operator

Emirates Waste to Energy Company (EWTE) - Bee'ah / Tadweer Group 50:50 JV

Status

Operational since May 2022 under a JV / DBOOM

Tariffs

Undisclosed

Serves

SEWA grid

The region's first commercial-scale Waste-to-Energy plant. Masdar exited its 50% stake to Tadweer Group in July 2025

A mega WtE expansion proposal re-engineered to 3,000 t/d (~1 Mt/y), ~QR 2bn (~USD 550M) indicative, is under government evaluation as of November 2025

How a WtE plant fits in the city waste cycle

A high-level view of how municipal solid waste (MSW) moves from households into a WtE plant and where the energy + residual streams go.

How a mass-burn WtE plant works

From refuse-truck tipping bay to stack and grid in six steps. Click any step for detail.

Click any step in the flow above

Each step opens a short description here. The same six-step backbone runs in every mass-burn WtE plant - what differs between deals is grate vendor (Martin / CNIM / Kanadevia Inova / Keppel Seghers), flue-gas treatment philosophy, and whether the heat is co-exported as district hot water.

WtE process technologies

Technology

What it is

How often it is used

Mass-burn moving grate

Industrial-scale reciprocating or roller-grate combustion. Handles mixed unsorted MSW with minimal preprocessing - the workhorse globally. Used at Sharjah (Martin / CNIM), Warsan (Kanadevia Inova / HZI), Al Bihouth (HZI) and Mesaieed (Keppel Seghers)

Most used

Anaerobic digestion + RDF

The organic fraction is anaerobically digested to biogas; the dry fraction is shredded into refuse-derived fuel (RDF) for combustion. A hybrid route for mixed waste streams and a fit for cement-kiln co-firing. Envisioned for the Saudi SIRC integrated PPP

Sometimes used

Gasification

Sub-stoichiometric heating produces a synthesis gas (CO + H₂) that is then burned in a separate combustion chamber or fed to an internal-combustion engine. Cleaner emissions but unproven at commercial GCC scale. Considered for Kabd Kuwait, where mass-burn was ultimately selected

Rarely used

Fluidised-bed combustion

Waste is shredded to ~50 mm pieces and burned in a hot sand bed held in turbulent suspension by upward-blown air. Better suited to RDF than unsorted MSW. Lower capex per t/d but lower availability. Not used commercially in the GCC

Rarely used

What is a Hazardous Waste plant?

A Hazardous Waste Treatment plant handles wastes that are toxic, corrosive, flammable, reactive, infectious or otherwise unsafe for ordinary disposal - industrial solvents, paint sludges, contaminated soils, used oil, e-waste, expired pharmaceuticals, lab chemicals, asbestos, refinery slops, oily drill cuttings, batteries, healthcare clinical waste. The plant exists to break these streams down into inert residues that can safely go to a secure landfill, recover useful materials (solvents, oils, metals), or destroy persistent organics by high-temperature combustion.

Hazardous-waste facilities are tightly licensed: in the GCC they typically operate under Environment Agency Abu Dhabi (EAD), SEPCO/MEWA (Saudi), EPA Bahrain or MECA Oman permits, with separate streams handled in separate trains. Incineration is at 1,100-1,200 °C with >2 seconds residence time (vs ~850 °C for municipal WtE) to destroy POPs and dioxin precursors. Flue-gas treatment is more aggressive - typically dry sorbent + activated carbon + baghouse + wet scrubber + SCR.

How a hazardous-waste plant fits the industrial waste cycle

The plant sits between the hazardous-waste generators (refineries, factories, hospitals, labs) and the final disposal points (recovered materials, secure double-lined landfill). Every load arrives on a licensed-hauler manifest.

How a hazardous-waste plant works

From licensed-hauler tipping to inert residue in six steps. Click any step for detail.

Click any step in the flow above

Each step opens a short description here. Unlike municipal WtE, a hazardous-waste plant runs several parallel treatment trains - rotary-kiln incineration for organics, physico-chemical for aqueous wastes, stabilisation for inorganic solids. The flow shown is the high-temperature incineration train.

Hazardous-waste treatment technologies

Technology

What it is

How often it is used

Rotary kiln incineration

Refractory cylinder + post-combustion chamber

Refractory-lined rotating cylinder followed by a post-combustion chamber held above 1,100 °C with >2 s residence time. Handles every physical form (solid, liquid, packaged, sludge). The workhorse of integrated GCC HW plants.

Neutralises acid/alkali, oxidises cyanide or reduces hexavalent chrome, precipitates heavy metals, then filter-presses the sludge for stabilisation. For aqueous and inorganic streams that should not burn.

Often used

Stabilisation / solidification

Cement-encapsulation of residues

Cement, lime or pozzolan binders lock mobile heavy metals and POPs into a monolithic solid before secure-cell landfilling. Mandatory for fly ash and APC residue from the incinerator.

Most used

Autoclave for medical waste

Steam at 134 °C / >3 bar

Steam sterilisation followed by shredding. Renders clinical waste safe for ordinary landfill or co-firing in WtE. Lower cost and emissions than incineration; not effective on cytotoxics.

Sometimes used

Plasma arc gasification

DC plasma torch at >3,000 °C

DC plasma torch vitrifies inorganics into an inert glass slag while organics gasify to syngas. Mature for asbestos and APC residue but capital-intensive. Niche role globally.

Rarely used

Real-world examples

Operational and announced facilities in the GCC. Where a site-specific photo is not yet on file, a placeholder is shown.

Photo pending

BeAAT - Al Ain

BeAAT - Al Ain UAE

Service

Integrated HW + medical

Technology

Rotary kiln + physico-chemical + secure cell

Operator

Tadweer

Status

Operational

The region's largest licensed hazardous-waste site - serves the UAE refining, manufacturing and healthcare sectors.

Photo pending

SIRC Riyadh hazardous

SIRC Riyadh hazardous Saudi Arabia

Service

Central HW for industrial Riyadh + Yanbu

Technology

Incinerator + stabilisation + secure cell

Operator

Saudi Investment Recycling Co (SIRC)

Status

Operational / expanding

Saudi Arabia's hazardous-waste consolidation platform, anchored by SIRC under PIF.

Photo pending

Veolia / Sehati

Veolia / Sehati Bahrain

Service

Medical-waste treatment

Technology

Autoclave + small incinerator

Capacity

~10 t/d

Status

Operational

The default hazardous facility for Bahrain's healthcare sector and small-island industrial users.

Photo pending

be'ah hazardous

be'ah hazardous Oman

Service

National HW programme

Technology

Rotary kiln (EOI 2023) + secure landfill

Operator

be'ah

Status

Procurement

Oman's national hazardous-waste rollout, with the secure landfill cell at Al Multaqa.

What is a Material Recovery & Organic Facility?

A Material Recovery Facility (MRF) is a mechanical sorting plant that pulls recyclable materials - paper, card, PET, HDPE, glass, aluminium and steel - out of mixed or commingled household waste using a sequence of screens, magnets, eddy-current separators, near-infrared optical sorters and air classifiers. An Organic facility is the parallel train for the biodegradable fraction: source-separated food and garden waste is composted (with or without anaerobic digestion first) into a marketable soil conditioner or used to produce biogas.

The two are usually combined on one site because a clean recyclate yield depends on diverting the wet organic fraction upstream, and because the organic train's screened reject becomes useful refuse-derived fuel (RDF) for the WtE or cement-kiln next door. In the GCC, MRF + Organic facilities are core to the circular-economy targets in Saudi Vision 2030, UAE Net Zero 2050 and Oman Vision 2040 - the goal in each country is 60-90% diversion from raw landfill.

How an MRF + Organic facility fits the city waste cycle

The plant sits between source-separated household collection and the downstream recyclate / energy markets. Its job is to split mixed waste into three high-value streams (recyclate, biogas + compost, RDF) and leave only a small inert residual for landfill.

How an MRF + Organic facility works

From tipping floor to baled recyclate and matured compost in six steps. Click any step for detail.

Click any step in the flow above

Each step opens a short description here. A well-designed MRF + Organic facility runs at 30-45 t/h throughput, achieving 60-80% input diversion to recovered streams. Plant economics depend critically on recyclate market price (especially PET and aluminium) and on the cleanliness of the source-separated feed.

MRF + Organic processing technologies

Technology

What it is

How often it is used

Trommel + ballistic sort

Mechanical pre-sort by size and shape

A rotating trommel screen splits feed by size; a ballistic separator splits 3D containers from 2D paper/film by bounce angle. Cheap, durable, and the backbone of every commingled-recyclables line in the GCC.

Most used

NIR optical polymer sorting

Hyperspectral imaging + air-jet ejection

Near-infrared scanners read each fragment's polymer fingerprint at 1,000+ scans/s; air-jet manifolds eject PET, HDPE, PP, LDPE, paper into dedicated chutes at >92% purity. Cannot see black plastics.

Often used

Eddy-current non-ferrous separator

Rotating magnetic rotor

A high-frequency magnetic rotor induces eddy currents in non-ferrous fragments; the resulting repulsion launches them off the belt. Recovery >85% for aluminium on a dry feed.

Most used

Wet anaerobic digestion

Mesophilic 35-40 °C reactor

Source-separated food waste digests over 18-25 days into biogas (~60% CH4) and digestate. Biogas is upgraded to biomethane and injected to the grid, or burned in a CHP engine. Best energy yield per tonne of organic.

Often used

In-vessel composting

Aerobic tunnels at 55-65 °C

Aerobic biological breakdown in enclosed tunnels for 14 days followed by windrow maturation. Tolerates higher contamination than AD; lower capex; output is compost only, no biogas.

Sometimes used

RDF / SRF production

Shred + dry + pelletise the reject

High-CV reject (paper + film + textiles) is shredded, dried and pelletised into refuse-derived fuel for the local WtE or cement kiln. Adds a fourth marketable stream and closes the diversion loop.

Often used

Real-world examples

Operational and announced facilities in the GCC. Where a site-specific photo is not yet on file, a placeholder is shown.

Photo pending

Dubai Municipality MRF

Dubai Municipality MRF UAE

Service

Commingled-recyclables sort

Technology

Trommel + ballistic + NIR + eddy-current

Operator

Dubai Municipality

Status

Operational

Large commingled MRF in Al Aweer - sorts post-consumer recyclables into baled output streams for converters.

Photo pending

Bee'ah MRF

Bee'ah MRF UAE

Service

MSW + C&D + tyre sort lines

Technology

Multi-line MRF

Operator

Bee'ah / EWTE

Status

Operational - feeds Sharjah WtE

High-throughput MRF on the Bee'ah Eco-Park; its high-CV reject feeds the adjacent Sharjah WtE Phase 1 line.

Photo pending

SIRC Organic pilot

SIRC Organic pilot Saudi Arabia

Service

Source-separated food-waste AD

Technology

Mesophilic anaerobic digestion

Operator

SIRC

Status

Pilot operating

Anaerobic-digestion pilot for source-separated food waste in Riyadh - biogas to grid, digestate to compost.

Photo pending

DSWMC Mesaieed AD

DSWMC Mesaieed AD Qatar

Service

Organic fraction of MSW

Technology

Anaerobic digesters co-located with WtE

Capacity

~200 t/d feed

Status

Operational

Anaerobic digesters integrated with the Mesaieed Waste-to-Energy site; biogas co-fired in the WtE boiler.

What is an engineered sanitary landfill?

A sanitary landfill is the regulated, engineered final disposal point for the residual waste that cannot be recycled, composted or burned. Unlike open dumping (which historically dominated the GCC), a sanitary landfill has a low-permeability composite base liner (clay + HDPE geomembrane), a leachate collection and treatment system, methane gas capture (often with power generation), daily soil cover to suppress odour and pests, and a long-term capping + post-closure monitoring obligation that runs 30 years after the final tonne is received.

In the GCC, sanitary landfills are being built (or retrofitted) to handle the inert residual from upstream MRFs and WtE plants, and to receive stabilised hazardous waste in segregated double-lined cells. The transition from open dumps to engineered landfills is one of the largest single capex lines in Tadweer, be'ah, Bee'ah, SIRC, MEW Kuwait, MMUP Qatar and SCE Bahrain investment plans. Lifespan of a typical engineered cell: 20-40 years before closure.

How an engineered landfill fits the city waste cycle

An engineered landfill is the terminal step of the waste hierarchy - it receives only the residual that cannot be recycled, composted or burned. Its job is to isolate that residual from groundwater for centuries, capture the methane it generates and treat the leachate that drains through.

How an engineered landfill works

From weighbridge to capped cell with post-closure monitoring in six steps. Click any step for detail.

Click any step in the flow above

Each step opens a short description here. A modern engineered landfill is not a passive hole - it's a managed slow-rate bioreactor that controls leachate, captures methane, and isolates contaminants from groundwater for centuries.

Landfill technologies

Technology

What it is

How often it is used

Engineered sanitary landfill

Composite liner + leachate + gas capture

Base liner: 0.5-1.0 m clay + 2 mm HDPE geomembrane + geotextile + 0.3 m drainage gravel. Leachate drains by gravity to a sump; gas wells feed a flare or engine. Default for all new municipal cells.

Most used

Landfill gas-to-energy (LFGTE)

Vertical gas wells + generator engine

Vertical wells and horizontal collectors feed a 1-5 MW gas engine that powers site loads or exports to the grid. Carbon credits possible under VCS / Gold Standard methodologies.

Often used

Secure hazardous landfill cell

Double HDPE liner + leak detection

Double HDPE liner with a leak-detection layer between, restricted access, segregated drainage. Receives only stabilised / cement-encapsulated hazardous residues.

Often used

Open-dump closure & cap

Regrade + multi-layer cap

Retrofit of legacy unlined dumps: regrade slopes, install passive gas vents, place geomembrane + drainage + soil cap. The old-site liability programme across GCC.

Sometimes used

Bioreactor landfill

Leachate recirculation

Leachate is recirculated through the waste mass to accelerate anaerobic decomposition - doubles gas yield, shortens stabilisation from 30+ years to 5-10. Requires very tight gas capture.

Rarely used

Real-world examples

Operational and announced facilities in the GCC. Where a site-specific photo is not yet on file, a placeholder is shown.

Photo pending

Al Dhafra landfill

Al Dhafra landfill UAE

Service

Municipal + stabilised residual

Technology

Composite liner + leachate plant + LFG flare

Operator

Tadweer

Status

Operational

Tadweer's flagship engineered landfill - receives stabilised residual from BeAAT and the Al Bihouth WtE.

Photo pending

Al Multaqa

Al Multaqa Oman

Service

National landfill consolidation

Technology

Sanitary cells + segregated hazardous cell

Operator

be'ah

Status

Operational - replacing ~300 open dumps

be'ah's national consolidation site, replacing legacy unlined dumps across Oman.

Photo pending

Mesaieed landfill

Mesaieed landfill Qatar

Service

Residual after WtE + AD

Technology

Sanitary cell + LFG flare

Operator

Domestic Solid Waste Management Centre

Status

Operational

Integrated site - sanitary landfill next to the Mesaieed WtE and AD plants.

Photo pending

Kabd cluster

Kabd cluster Kuwait

Service

Greater Kuwait MSW residual

Technology

Engineered cells + planned LFGTE

Operator

Kuwait Municipality

Status

In rollout

Long-term consolidation cluster around Kabd, replacing pre-2000 dumps.

What is sludge incineration?

A sludge incineration plant burns dewatered sewage sludge - the solid by-product of every Sewage Treatment Plant (ISTP) - at 850-950 °C in a fluidised-bed furnace. Each m³ of treated sewage produces ~0.5-0.7 kg of dry sludge cake (25-30% dry-solids after centrifuge or belt-press dewatering); a city of 1 million people generates 150-200 t/d of cake. Without incineration, this cake either goes to landfill (where it consumes airspace and emits methane) or to agricultural reuse (limited by salinity / pathogen / heavy-metal constraints in the GCC).

Incineration reduces the sludge to ~10% of its original mass as a sterile inert ash, recovers the sludge's residual calorific value (~10-12 MJ/kg DS) to dry incoming cake, and - in larger plants - exports modest electricity (3-8 MW) or process heat. It is conceptually adjacent to Waste-to-Energy but distinguished by a very different feedstock (homogenous, high-moisture, high-ash) and by smaller scale (typical 100-400 t/d cake per plant vs 1,000-5,000 t/d for municipal WtE). In the GCC, sludge incineration becomes attractive as the installed ISTP base grows - the natural co-location is alongside or downstream of an ISTP cluster.

How a sludge-incineration plant fits the sewage cycle

The plant sits downstream of every major ISTP, taking the dewatered cake the plant cannot recycle. Its job is to dry that cake, burn it in a fluidised bed, recover the heat to dry the next batch, and leave only a sterile inert ash.

How a sludge-incineration plant works

From dewatered cake silo to sterile ash and exported heat in six steps. Click any step for detail.

Click any step in the flow above

Each step opens a short description here. Sludge incineration is the smaller cousin of municipal WtE - similar combustion principles, very different feedstock characteristics (high moisture, high ash, low LHV), and a strong dryer/boiler/incinerator energy loop that defines plant economics.

Sludge-incineration technologies

Technology

What it is

How often it is used

Bubbling fluidised bed (BFB)

Hot sand bed at modest air velocity

Hot sand bed suspended by primary air at modest velocity. Simple, robust, autothermal above ~35% dry-solids feed. The default modern choice for dedicated sludge incinerators at 100-500 t/d.

Most used

Circulating fluidised bed (CFB)

Bed solids entrained + recycled

Higher gas velocity entrains bed solids, which a cyclone returns to the bed. Better turn-down and load-following, slightly higher capex. Used for larger or fuel-variable plants.

Often used

Co-incineration in a WtE plant

Dewatered sludge fed at <5-10% of WtE feed

Cake is fed at <5-10% of the municipal WtE feed. Cheap (no dedicated plant) and uses existing flue-gas treatment, but caps the sludge share and competes with MSW airspace.

Sometimes used

Cement-kiln co-firing

Dried sludge as alternative fuel

Dried sludge is fed as an alternative fuel into clinker kilns at 1,400 °C. POPs are destroyed; the ash is locked into the clinker. Constrained by cement-plant siting and licensing.

Sometimes used

Multiple-hearth furnace

Stacked refractory hearths (legacy)

Stacked refractory hearths with rotating rabble arms. 1960s-80s legacy technology; tolerates lower DS feed but worse emissions control. Being phased out globally.

Rarely used

Real-world examples

Operational and announced facilities in the GCC. Where a site-specific photo is not yet on file, a placeholder is shown.

Photo pending

Riyadh central sludge

Riyadh central sludge Saudi Arabia

Service

Centralised sludge for Riyadh ISTP cluster

Technology

Bubbling fluidised bed (planned)

Operator

SIRC + SWPC programme

Status

Concept / planned

Centralised sludge incinerator serving the Riyadh ISTP cluster - concept stage in the SIRC + SWPC integrated waste programme.

Photo pending

Abu Dhabi STEP sludge

Abu Dhabi STEP sludge UAE

Service

STEP ISTP cluster sludge

Technology

Fluidised-bed incinerator (studied)

Operator

EWEC / Tadweer (studied)

Status

Feasibility

Studied add-on to the Strategic Tunnel Enhancement Programme (STEP) ISTPs - would replace the present land-applied biosolids route.

Photo pending

Warsan WtE co-firing

Warsan WtE co-firing UAE

Service

Sludge co-fired with MSW

Technology

WtE moving grate (existing) + sludge feed

Operator

Dubai Municipality / WPA

Status

Studied

Smaller sludge volumes can co-fire at the existing Warsan or Sharjah WtE - cheaper than a dedicated plant but caps the sludge share at ~5-10% of feed.

Photo pending

LafargeHolcim cement-kiln

LafargeHolcim cement-kiln GCC

Service

Dried sludge as alternative fuel

Technology

Cement clinker kiln at 1,400 °C

Operator

LafargeHolcim / Cemex GCC

Status

In use at multiple sites

Dried sludge as an alternative fuel in cement clinker kilns - POPs destroyed at 1,400 °C, ash locked into the clinker. Already in commercial use.

Database

Combined GCC waste-management PPP benchmark - all sub-types in one table. Filter by Type to switch between Waste-to-Energy, Hazardous, MRF & Organic, Landfill and Sludge incineration. Gate-fee and capex charts focus on Waste-to-Energy entries where the tariff and MW concepts apply.

Map - GCC Waste Management

All sub-types · marker colour = waste type · scroll to zoom, click a marker for project details

1 Final gate fee against plant throughput

Awarded GCC WtE PPPs · USD/t gate fee against waste throughput (t/d), categorised by procurement era

2 Bigger plants cost less per kilowatt - economies of scale

Build cost per kW of electricity output against plant size (MW) · country-coloured bubbles, dashed line is the power-law scale trend

3 Who is winning the market - sponsor participation

Tracked throughput per sponsor · every named consortium member counted on each deal they won

4 Where the market is - by country

Tracked throughput and project count by country

5 Process technology mix

Treatment process by project · mass-burn grate / fluidised bed / gasification / AD + RDF

6 Concession term length

Concession years by project · where the PPA / WtE term is publicly disclosed

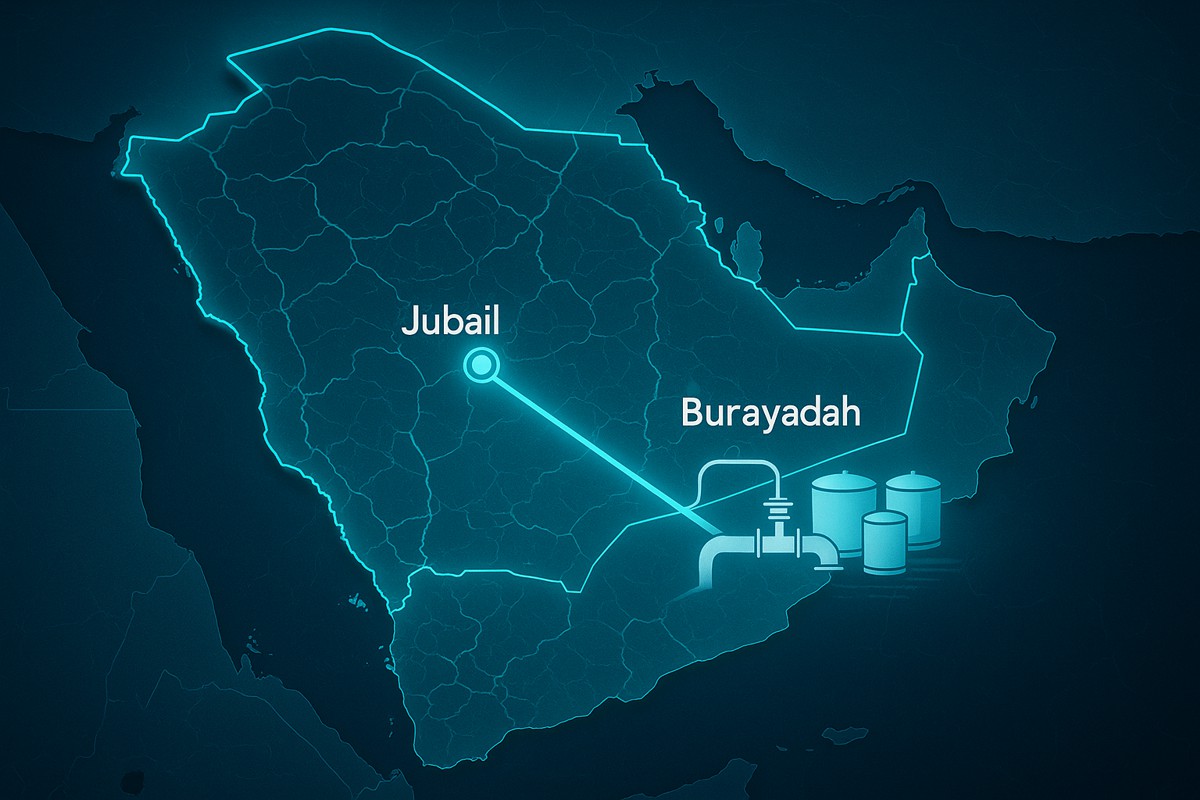

An Independent Water Transmission Pipeline (IWTP) is a buried steel water main, hundreds of kilometres long, that carries desalinated drinking water from a coastal SWRO plant to inland cities. Pump stations every 60-80 km along the route push the water forward and uphill (Saudi inland cities sit 600+ metres above sea level). Strategic storage tanks at the destination cities hold multi-day water reserves.